The Importance of Diversification: Spreading the Risk

Don’t Let One Bet Define Your Outcome

“Never test the depth of the river with both feet”, Warren Buffett cautioned; a reminder that overconfidence in a single investment can be costly.[1] Behavioral finance shows that humans are prone to recency bias, chasing last year’s winners and underestimating the possibility of sudden reversals.

Consider the investor who puts everything into a single “can’t-miss” stock or sector. When that bet pays off, the rewards can be outsized. But when the tide turns, losses can be swift and severe. History is littered with examples: from the tech bubble to the financial crisis, concentrated portfolios have often magnified pain during downturns.

Diversification isn’t about diluting conviction; it’s about acknowledging the limits of foresight. By spreading investments across asset classes, sectors and geographies, the risk is reduced that any one event can derail your financial goals. The result is a portfolio that is more resilient, less vulnerable to shocks and better positioned for long-term growth, even if you don’t “know” what’s coming next.

[1] Warren Buffett Quotes: 10 of My Favorites: TheCorporateCounsel.net Blog

What is Diversification

Diversification is the practice of spreading investments across different asset classes, sectors and regions. Effective diversification goes beyond just having many holdings. It’s about choosing investments with different drivers. Instead of relying on one stock or market, blended assets may react differently to economic events.

A well-diversified portfolio could include various:

- Asset classes: Stocks, bonds, real assets and alternatives

- Geographies: U.S. and international markets

- Sectors: Technology, healthcare, energy and more

- Styles: Growth vs. Value, for example

The key is correlation: choosing investments that don’t all move together. When one area struggles, others may hold steady or even rise, helping to smooth out returns over time.

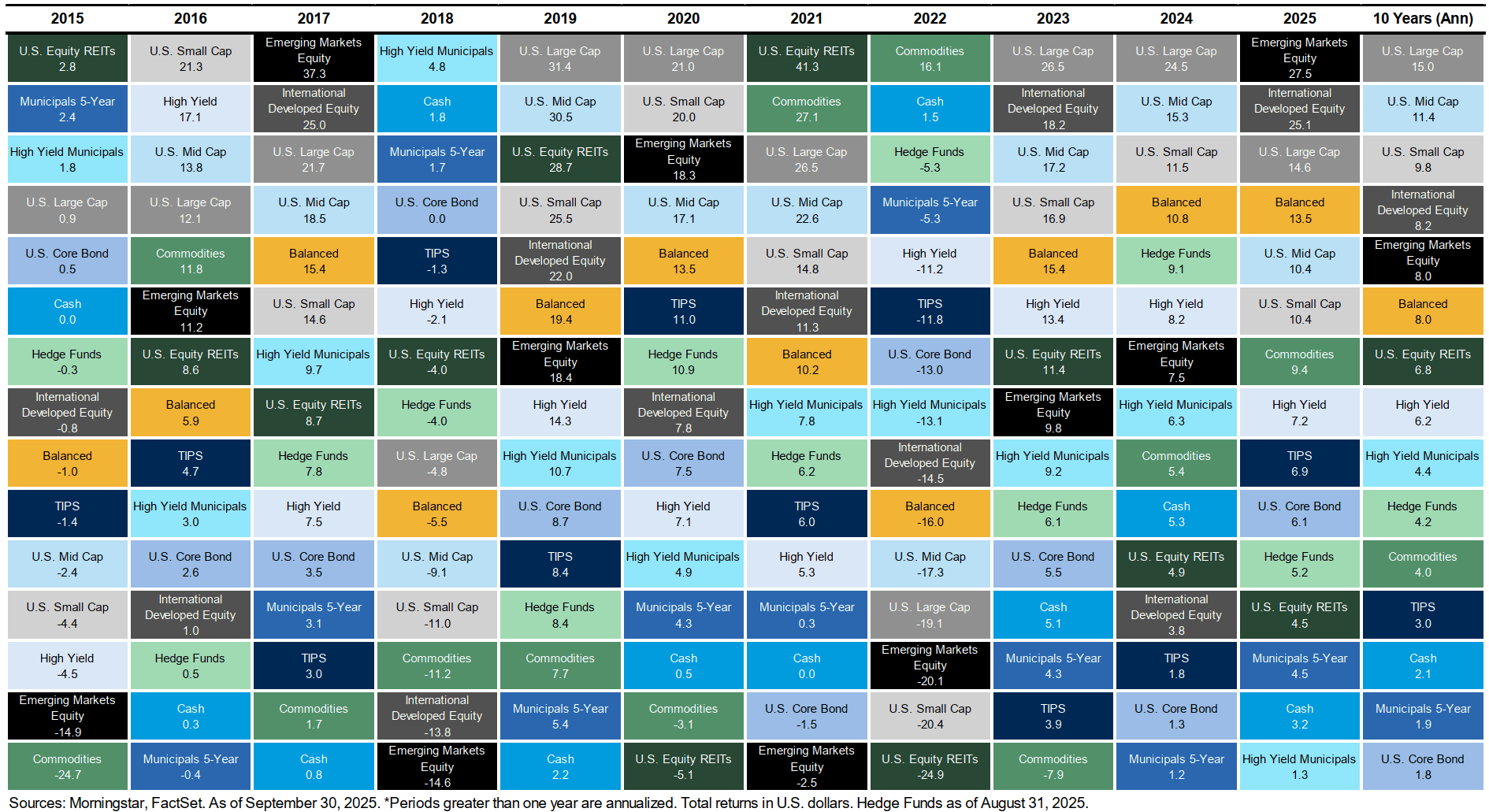

Below, note how the leaders and laggards change each year. No single asset class consistently outperforms – diversification matters.

Three Potential Benefits of Diversification

Behavioral differentiator

Less whiplash supports better decisions. By reducing the frequency and severity of “gut-check” moments, diversification helps investors stick to policy, rebalance on schedule, stay invested and avoid costly market-timing mistakes that arise when volatility bites.

Efficiency

Diversification can improve risk-adjusted returns, the return received for each unit of risk, by combining assets so the whole is more efficient than the parts. Combining assets with different risk/return profiles and correlations can place a portfolio closer to the efficient frontier, where you either take less risk for the similar return or seek more return for similar risk. It’s the portfolio-level benefit that security-by-security thinking can miss.

Resilience

By spreading investments across regions and sectors, a portfolio is built with the goal to withstand surprises. Whether it’s a sudden policy change, a market shock or a natural disaster, diversification helps ensure that no single event derails your financial goals.

What Diversification is Not

Diversification doesn’t mean your portfolio is immune to losses. It may help reduce the risk of any single investment hurting your results, but it can’t shield you from broad market declines or systemic shocks. It’s not a one-time fix, either. As asset correlations and market trends shift, a diversified portfolio needs ongoing attention. Without regular rebalancing, your mix can drift and lose its protective benefits.

And more isn’t always better. When too many similar investments are added, one may think they’re spreading risk. In reality, overlapping holdings can concentrate risk in disguise. Effective diversification is about thoughtful selection, not just quantity.

Putting it to Work: A Practical Checklist

Start with objectives & constraints.

Clarify purpose, time horizon and liquidity needs (emergency cash, near-term withdrawals). Align risk tolerance with what you can financially and emotionally withstand.

Build the core.

Use broad, low-cost building blocks across equities, bonds and real assets, where suitable. Favor diversified index or core funds to capture market beta efficiently before adding complexity. Keep position sizes meaningful and avoid overlapping that could add cost without new risk or return exposure.

Add diversifiers thoughtfully.

Introduce non-U.S. and small/mid-cap exposures to broaden opportunity, where suitable. Value/quality tilts, inflation-aware and tax-advantaged income are also helpful diversifiers.

Rebalance on a cadence or band.

Choose rules you’ll follow in good and bad markets. Examples: calendar-based (quarterly/annual) or band-based (rebalance when weights breach set thresholds) to enforce buy-low/sell-high behavior.

Consider costs & taxes.

Benchmark every holding’s expense ratio against lower-cost alternatives. Keep in mind after-tax strategies like asset location, tax-loss harvesting and minimizing realized short-term gains, so every basis point supports your objective.

Common Questions About Diversification

How many funds do I need?

Focus on capturing distinct sources of return, different asset classes, regions and styles. More tickers don’t always mean more diversification; overlapping holdings can recreate the same risk.

What if everything falls at once?

During market stress, correlations can spike and even diversified portfolios may decline together. The goal is to reduce risk concentration, not eliminate risk. Diversification can help cushion the impact, but it cannot prevent all losses.

When should I adjust?

Review your portfolio when your goals, timeline or risk tolerance change. Otherwise, stick to your rebalancing policy, adjusting only when allocations drift outside set bands or on a regular schedule.

Do I need alternatives (private credit, hedge funds, etc.)?

Only if they serve a clear role (income, diversification outside traditional public equities) and you accept illiquidity, fees and complexity.

How much cash should I keep?

This will vary per investor. Generally, keep near-term needs (e.g., 6–12 months of spending) in cash or cash equivalents so long-term assets can stay invested.

Conclusion

Don’t let recency bias or overconfidence steer your investment journey. It’s tempting to chase last year’s top performing asset, assuming the trend will continue. Markets are cyclical, and yesterday’s winners can quickly become tomorrow’s laggards. By diversifying, you avoid putting all your faith in a single story and give yourself a better chance to capture returns across different environments. Clients of MPS LORIA who utilize firm allocations have proper asset allocation, Manager/strategy due diligence and proactive risk and strategic rebalancing performed routinely by the firm. It is a core part of successful investing on all types of markets.

Past performance does not indicate future performance and there is a possibility of a loss. This report is intended for the exclusive use of clients or prospective clients of MPS LORIA. The information contained herein is intended for the recipient, is confidential and may not be disseminated or distributed to any other person without the prior approval of MPS LORIA. Any dissemination or distribution is strictly prohibited. Information has been obtained from a variety of sources believed to be reliable though not independently verified. Any forecasts represent future expectations and actual returns; volatilities and correlations will differ from forecasts. This report does not represent a specific investment recommendation. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice.